Click Here for MCQs Practice Based on Specialised Accounting

Accounting for Non-Trading Organisations

INTRODUCTION

Receipts and Payments Account, Income and Expenditure Account, and Balance Sheet are typically prepared by non-profit organisations such public hospitals, public educational institutions, clubs, etc. to indicate periodic performance and financial position at the conclusion of the accounting period.

In this unit, we'll talk about how to create a balance sheet, income and expense account, and receipts and payments account for nonprofit or non-trading organisations. Additionally, we'll go through and show how to create an income and expense account from a receipts and payments account. It should be noted that the profit and loss account created for profit-making organisations is very similar to the income and expense account.

The excess of expenditure over income in an income and expense account is seen as a surplus.Total cash payments and receipts are highlighted in non-profit organisations' receipts and payments accounts.

Meaning of Non-trading Organisations:

The term "non-trading organisations" refers to businesses whose primary goals are to serve its members and the community rather than to make a profit. These groups are dedicated to advancing social welfare. The distribution or payment of dividends is prohibited by their charters. Sports teams, social groups, educational institutions, libraries, hospitals, religious trusts, temples, churches, mosques, gurudwaras, and other similar organisations are examples of such organisation.

Characteristics of Non-trading Organisations:

- The main objective of such concern is not to earn profit but providing services to its members and society.

- The main sources of revenues are Subscriptions money and Donation donations from member and societies

- A non-profit organisation is governed and managed by elected member in the same way a business corporation is managed by a board of director.

- A non-profit organization employs the same accrual basis of accounting used by business enterprises.

- Non Profit Organisations prepare receipts and payments account, income and expenditures account and balance sheet.

Accounting procedures of Non-trading Organisation

Non-trading organizations can keep and maintain their accounting records under single entry system or double entry system. The small sizes of organizations follow single entry whereas the large size of organizations follow double entry system. A Non Trading organisation prepares at the year end, the following three financial statements:

A. Receipt and payment account

B. Income and expenditure account

C. Balance sheet

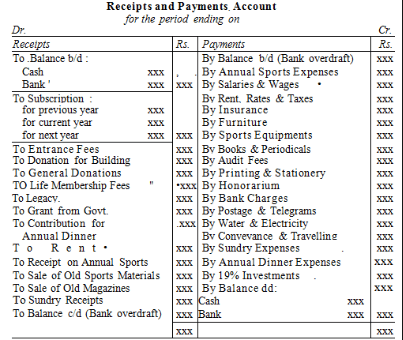

Meaning of receipt and payment account

It is summary of cash receipts and cash payments. It is real account. At the conclusion of the accounting period, it is prepared. On the debit side of the receipts and payments account, all cash receipts are recorded, and on the credit side, all payments are recorded.

The receipts and payment are a summary of all cash receipts and payments, whereas the cash book is made up of entries of receipt and payment in chronological order. A receipt and payment account begins with the opening cash and bank balance and finishes with the closing cash and bank balance. It does not account for any unpaid balance in the receipts and payments account. Payments and receipts could be of a capital or revenue type. These could be connected to the If they are actually received or paid, they must show up in this account whether it is the current, previous, or following year.

Characteristics of receipts and payment account:

The main characteristics or attributes are as follows:

It is a summary of cash transactions. Like a cash book records cash receipts on debit side and payments on the credit side.

It includes cash and banking transactions whether these are related with previous or current or subsequent yea ₹

It records all receipts and payments whether related to capital or revenue nature.

It starts with opening balance of cash in hand and cash at bank.

It ends with closing balance of cash in hand cash at bank.

It does not include non-cash transactions like Depreciation or outstanding expenses or revenue.

It is not based on accrual basis of accounting.

Limitations of receipts and payment account:

The limitations of receipts and payments are follows:

It is not able to find surplus and deficit of the organizations.

It does not account income and expenses on accrual basis.

It does not differentiate capital and revenue receipts and payments.

It does not record non-cash items such as depreciation or outstanding expenses.

Format of Receipts and Payment Account

Comments

Post a Comment

Thanks for your valuable comments